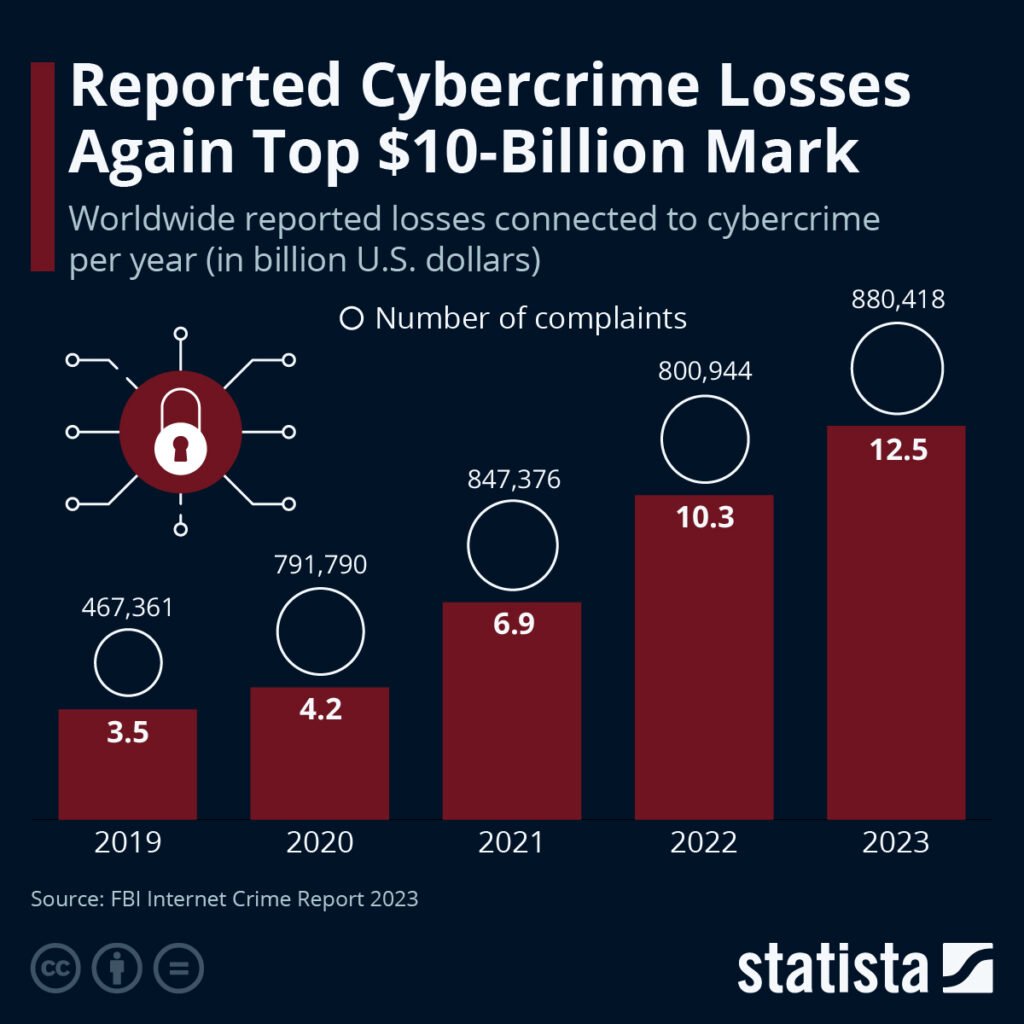

In the last few years, cyber scams have quietly grown from a background threat to a direct business risk. Most companies today understand that cyberattacks exist, but very few realise how easily these scams can drain money—not just in the form of stolen funds, but through a long chain of consequences that appear weeks or even months later.

When you talk to business owners, many think cybercrime is something that happens to “big brands,” or only to companies with poor security. But the truth is far more uncomfortable: even well-run businesses lose money every single day because of small, unnoticed cyber scams.

It usually begins with one odd email, a misdirected payment, an employee clicking something they shouldn’t have, or a customer database leak buried deep in a neglected server.

Let’s break down how companies are actually losing money, and why this topic demands urgent attention.

1. Direct Financial Theft—The Most Obvious Loss, But Not the Only One

The most visible way companies lose money is when scammers directly steal it.

This could be through:

A fraudulent invoice that looks almost identical to the real supplier

A fake payment link sent to an employee

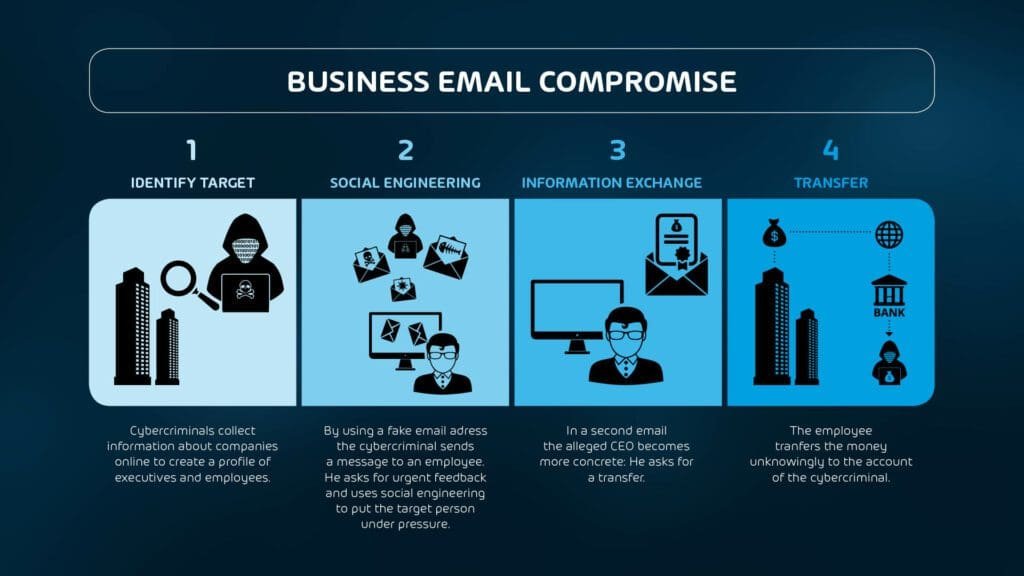

A spoofed CEO email pressuring someone in accounts to “make a quick transfer”

A hacked business email system used to divert payments

One midsize business recently shared how they lost ₹42 lakh simply because a scammer created an email ID one letter off from their vendor’s. The accounts executive didn’t notice, processed the payment, and the money disappeared overseas within minutes.

These attacks look simple, but they’re incredibly effective. And once the transfer is made, recovering the funds is extremely difficult. Banks try their best, but by the time the fraud is detected, the scammer has already split or withdrawn the money.

2. Ransomware Drains Money Even if the Ransom Isn’t Paid

Most people assume ransomware is only expensive if you actually pay the ransom. But companies lose money long before the ransom becomes a topic of discussion.

Imagine your systems lock up overnight. Employees can’t access customer files, orders stop processing, customer service queues pile up, and manufacturing lines halt.

Here’s where businesses actually lose money:

Every hour of downtime

Lost sales

Angry customers canceling orders

IT teams pulled off other work to focus only on recovery

Cost of forensic audits

Emergency security tools and consultants

For many companies, the real loss isn’t the ransom—it’s the business disruption. Some businesses spend more fixing the aftermath than the hackers demanded.

3. Loss of Customer Trust—Something You Cannot Put an Exact Number On

A data breach doesn’t just expose information; it affects how customers feel about your brand.

Customers today are very aware of privacy, especially after the DPDP Act and global data protection trends. If they learn that their email, phone number, or payment details were compromised, they naturally hesitate to shop or engage with that business again.

This silent churn is where many companies bleed money without realising:

Reduced repeat sales

Lower customer lifetime value

Higher marketing spend to regain trust

Bad reviews or negative press

A single breach can undo years of brand-building. And unfortunately, trust once broken is hard to rebuild.

4. Legal Penalties and Compliance Costs After a Breach

With laws tightening worldwide (including India’s DPDP Act 2023), companies now face heavy financial consequences if they fail to protect user data.

What many businesses don’t realise is that even a small cyber scam—like an email compromise—can lead to:

Legal investigations

Audits

Fines

Mandatory reporting

Expensive compliance upgrades

Even if the company did not intentionally violate anything, regulators often demand evidence of adequate security measures. If your systems were weak, the fine can be substantial, and the cost of compliance afterward becomes an ongoing expense.

5. Increased Operational Costs After an Attack

Cyber scams rarely end with “fixing the issue.” The biggest expenses often come afterward.

Companies may need to:

Upgrade their IT infrastructure

Invest in new cybersecurity software

Hire cybersecurity consultants

Train employees

Replace outdated hardware

Purchase cyber insurance

These are not one-time costs. Cybersecurity becomes a recurring operational budget—sometimes one that companies weren’t prepared for.

Even small businesses can suddenly see a 20–40% rise in tech spending after falling victim to a scam.

6. Employee Productivity Takes a Hit

When a scam occurs, it doesn’t just affect the IT team. Employees across departments lose precious time dealing with:

Account resets

Incident reporting

Security awareness refreshers

Manual workarounds while systems are restored

Investigations and interviews

This productivity drop can last days or weeks depending on the severity. And because the impact is spread across teams, companies often underestimate how much this costs them.

7. Damage to Business Partnerships

Many companies rely on suppliers, distributors, or financial partners. A cyber scam creates doubt in these relationships.

For example:

A vendor may demand stricter payment terms

A partner may insist on additional verification steps

Banks may increase monitoring or put holds on suspicious transactions

Insurance companies may hike premiums

These frictions slow the business down and increase long-term operational costs.

8. Loss of Intellectual Property and Confidential Data

Sometimes, scammers are not after immediate money—they want your ideas.

This includes:

Product designs

Pricing strategies

Business proposals

Market research

Client data

Proprietary software or algorithms

When competitors or malicious actors get access to this information, it can lead to long-term financial loss. You may lose bids, lose clients, or watch competitors replicate strategies you invested heavily to develop.

Why Are These Scams Increasing So Rapidly?

Three main reasons:

1. Scammers are using AI to create more convincing attacks.

Fake emails, voice clones, deepfake videos—everything looks scarily real.

2. Hybrid work has expanded the attack surface.

Employees working from phones, home Wi-Fi, or shared devices increase vulnerability.

3. Companies underestimate social engineering.

Most scams don’t break systems—they trick people.

This is why internal awareness is now as crucial as firewalls and antivirus tools.

How Companies Can Reduce These Losses

A few practical steps can dramatically reduce risk:

Conduct regular cybersecurity training

Implement 2-factor authentication everywhere

Use email filtering and anti-phishing tools

Verify payments through secondary confirmation

Maintain regular device and server updates

Back up data every week

Run mock phishing simulations

Invest in cyber insurance

Secure admin access and passwords

Cybersecurity doesn’t have to be expensive; inconsistent practices are what cost the most.

Final Thoughts

Cyber scams are no longer a distant threat—they’re an everyday business reality. Companies aren’t just losing money through stolen funds. They’re losing revenue, trust, productivity, and future opportunities without realising the full impact.

If your business hasn’t reviewed its cyber protection strategy recently, this is the right time. A small preventive step today could save you lakhs—or even crores—tomorrow.